We like to think money decisions are rational. In reality, most are fast, intuitive, and shaped by mental shortcuts that were useful in the wild but expensive in the markets. The good news is you do not need to erase your emotions to invest well. You need a system that recognizes predictable behavioral traps and routes you around them.

Below is a practical guide to the three biggest repeat offenders — loss aversion, anchoring, and herd mentality — plus a supporting cast of biases that often travel with them. You will get clear symptoms, simple diagnostics, and toolkits you can put to work today. Where helpful, I added tables to turn theory into action.

Part 1: The Patterns Behind “Why Did I Do That Again?”

1) Loss Aversion

What it is

Losses feel about twice as painful as equivalent gains feel good. Your brain treats “not losing” as safety, even when playing it too safe guarantees you fall short>

How it shows up

- You hold losers too long, waiting to “get back to even.”

- You sell winners too early and cut off compounding.

- You prefer guaranteed small gains over higher expected gains with mild volatility.

Portfolio impact

Under-allocation to growth assets, missed rebounds, tax-inefficient trades, and a performance drag from “zombie” positions.

Counter moves

- Decide exits in advance with predefined loss limits and time-based rules.

- Use rebalancing bands to trim strength and add to weakness in a controlled way.

- Frame outcomes in long-run probabilities rather than single outcomes.

- Automate contributions so you buy through bad headlines, not in spite of them.

2) Anchoring

What it is

Your first reference point becomes a mental “anchor.” You then adjust too little, even if the anchor is irrelevant.

How it shows up

- “This stock was ₹1,000 last year. It is cheap at ₹700.”

- “My property appreciated 20% last year. It will keep doing that.”

- You anchor to a past portfolio peak and judge every decision against it.

Portfolio impact

Chasing “cheap vs old high,” ignoring new information, and resisting portfolio changes when the world has changed.

Counter moves

- Swap price anchors for business anchors: cash flows, balance sheets, competitive position.

- Compare against base rates for the asset class, not last year’s price.

- Use decision memos that force “What would change my mind?” before you buy.

3) Herd Mentality

What it is

When uncertain, we copy the crowd to avoid social loss. Markets amplify it into fear at bottoms and greed at tops.

How it shows up

- Buying what is popular simply because it is popular.

- Selling only after everyone else already has.

- Performance-chasing funds or sectors.

Portfolio impact

Buying high and selling low. Overlap across funds. Concentration in the same stories the crowd owns.

Counter moves

- Pre-commit to asset allocation ranges and stick to rebalancing cadence.

- Maintain a watchlist with triggers based on fundamentals, not headlines.

- Conduct premortems: “It is 12 months later and this investment failed. What went wrong?”

Part 2: Your Bias Map

Use this table to quickly identify which bias is driving a decision and what to do next.

| Symptom you notice | Likely bias | Typical costly behavior | Quick diagnostic question | Practical fix |

| “I will sell when it gets back to my buy price.” | Loss aversion | Holding losers for too long | If I had cash today, would I buy this at this price? | Set exit rules by thesis, not entry price. Use time stops. |

| “It used to trade at 30x, so 25x is cheap.” | Anchoring | Valuing by old multiples | What is the base-rate multiple for peers today and why? | Re-anchor to forward cash flows and sector base rates. |

| “Everyone is rotating into X. I will miss out.” | Herd mentality | Momentum-chasing | Would I buy this if nobody I know owned it? | Allocate by policy. Rebalance on schedule. |

| “This stock is ‘house money’ after gains.” | Mental accounting | Risking gains more freely | Does the rupee know where it came from? | Treat all rupees identically. Re-underwrite position. |

| “I have a hunch. I am usually right.” | Overconfidence | Oversized positions, under-diversification | What is my error rate on similar calls? | Position-size with max risk per idea. Keep a track record. |

| “I have already spent so much time and fees.” | Sunk-cost fallacy | Throwing good money after bad | Would a new investor choose to continue this? | Ignore past costs. Decide only on future expected value. |

| “I can find a chart to prove it.” | Confirmation bias | Filtering out disconfirming data | What evidence would disprove my view? | Seek a “devil’s advocate.” Log both sides before acting. |

| “This 12-month return looks amazing.” | Recency bias | Extrapolating the latest run | Is the driver structural or cyclical? | Examine a full cycle. Use 5 and 10-year metrics. |

Part 3: Decision Architecture

Rather than relying on willpower, redesign the path of least resistance so the right behavior is automatic.

A) Your Personal Investment Policy (1-page)

Write it once. Follow it always.

Core elements

- Purpose: the “why” behind your money.

- Target allocation: equities, fixed income, international, alternatives.

- Risk guardrails: max drawdown you can tolerate, max position size, max illiquid exposure.

- Rebalancing rule: calendar based or band based.

- Security selection rules: what qualifies, what disqualifies, when to sell.

- Governance: who can overrule and under what conditions.

Template summary

| Section | What good looks like |

| Purpose | “Retire at 55 with inflation-indexed income covering ₹X per month and education corpus of ₹Y.” |

| Allocation | “60% equities, 30% high-quality debt, 10% diversifiers. Bands ±5%.” |

| Risk | “Max 10% in any single stock. Max 20% in illiquid assets. Maintain 6 months expenses in cash.” |

| Rebalance | “Quarterly or when any band breaches.” |

| Selection | “Positive free cash flow, acceptable leverage, durable moat, aligned management.” |

| Exit | “Thesis break, better opportunity, tax-loss harvesting, or rule-based trim on valuation extremes.” |

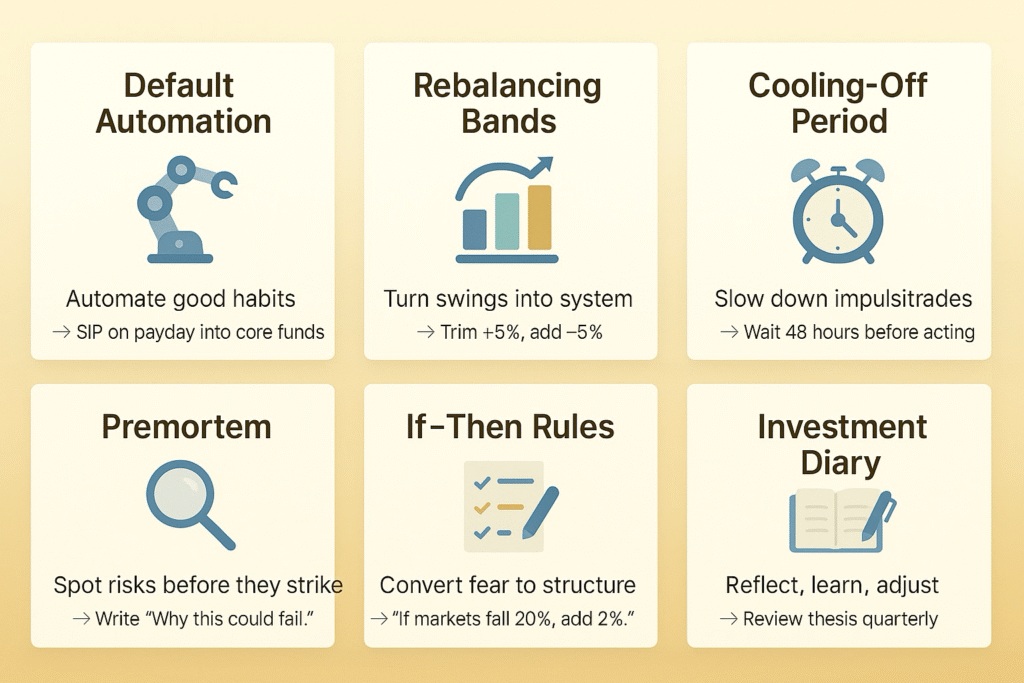

B) Pre-Commitment Toolkit

Make it easier to do the right thing at the right time.

| Tool | What it does | How to implement |

| Default automation | Removes timing from saving | Auto SIPs on payday into core funds or model portfolio. |

| Rebalancing bands | Turns volatility into discipline | Trim at +5% over target, add at −5% under target. |

| Cooling-off period | Slows down hot takes | Wait 48 hours before any discretionary trade. |

| Premortem | Surfaces hidden risks | Write “Why this could fail” before buying. |

| If–then rules | Converts fear into triggers | “If markets fall 20%, then add 2% to equities monthly for three months.” |

| Investment diary | Trains calibration | Record thesis, risks, and expected drivers. Review quarterly. |

Part 4: Worked Examples

Example 1: Anchoring to a Past High

You bought Stock A at ₹1,000. It is now ₹700 after a business stumble. Your mind says “wait for ₹1,000.”

Reframe with a decision memo

- Updated thesis: Has the moat eroded or is this fixable?

- Forward numbers: Expected free cash flow, growth, balance sheet.

- Base rate: What happened to peers after similar shocks.

- Action: Hold, add, or exit based on forward return vs other ideas, not the old price.

Result

You either upgrade the position because future returns look attractive or you rotate into a stronger opportunity, avoiding dead money.

Example 2: Loss Aversion During a Drawdown

Your equity sleeve is down 18%. You feel like stopping SIPs.

Reframe with bands

- Allocation target is 60% equities. After the drop it is 54%.

- Rule says add 2% when underweight by more than 5%.

- You top up gradually rather than guess the bottom.

Result

You convert pain into a rule-driven buy that shortens the recovery time.

Example 3: Herding Into a Hot Theme

A sector is up 60% year to date and every headline praises it.

Reframe with a premortem

- Valuation stretched, earnings sensitive to one variable, crowd crowded.

- You limit exposure to the policy max or use a staggered entry only if quality and cash flows justify it.

Result

You participate thoughtfully or you pass without regret because the choice came from policy, not FOMO.

Part 5: Quick Reference Tables

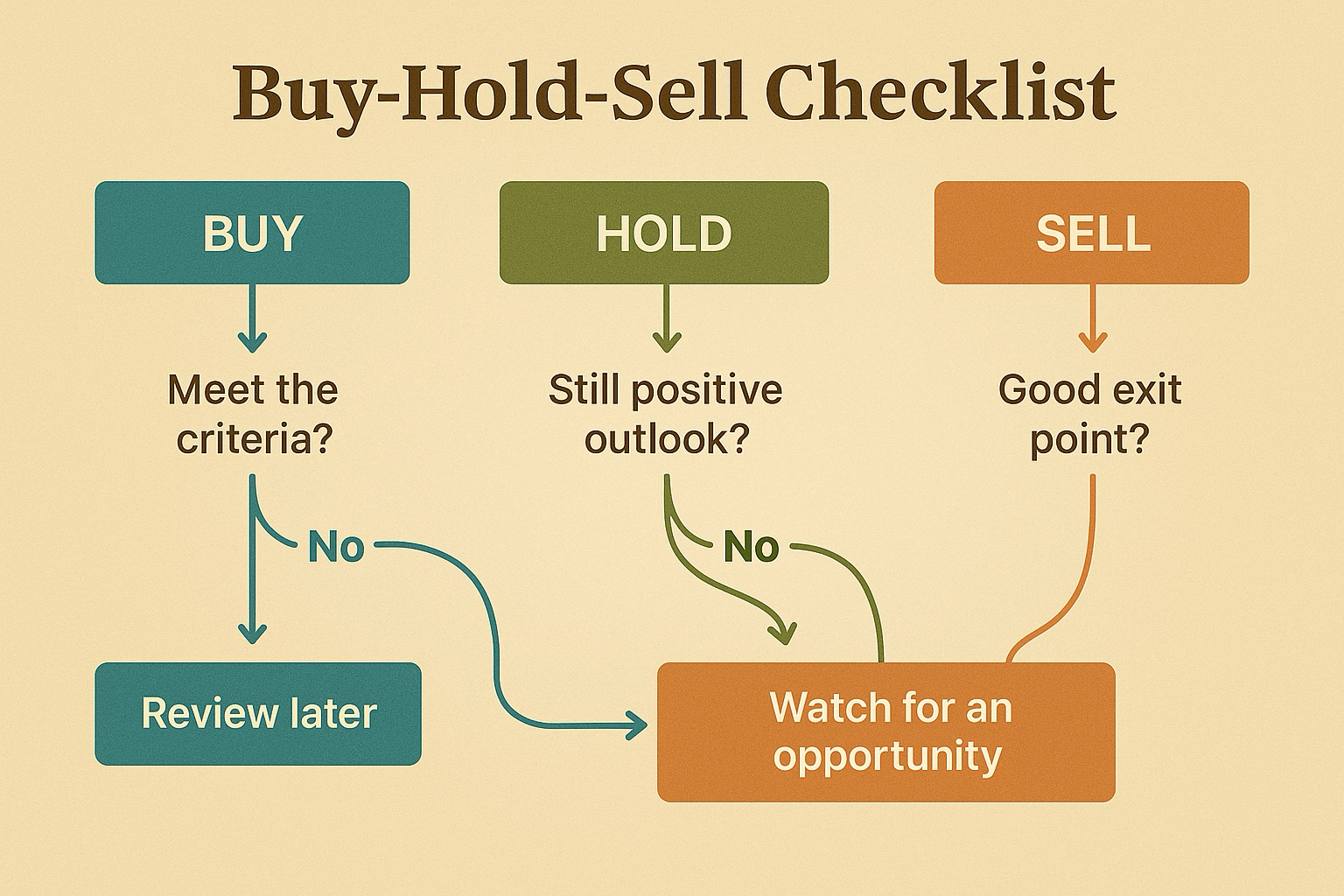

A) “Should I Buy, Hold, or Sell?” Checklist

Use before every trade.

| Question | If “No,” do this next |

| Do I understand how this business makes money? | Write a one-paragraph explanation. If you cannot, pass. |

| Is the balance sheet appropriate for the cycle? | Check leverage, covenants, refinancing needs. |

| Do forward cash flows justify today’s price range? | Build a simple scenario table. Require a margin of safety. |

| What would change my mind to sell? | Define two thesis-break triggers in writing. |

| Is this better than my next best idea? | Compare expected return per unit of risk. |

| Does this keep my portfolio within policy bands? | Rebalance first, then size position appropriately. |

B) Scenario Table for Discipline

A lightweight way to detach from price anchors.

| Scenario | Assumptions | 3-year outcome | Decision guide |

| Bear | Margin compresses, growth stalls | Low single-digit IRR | Avoid or tiny starter position |

| Base | Stable margins, mid growth | High single-digit IRR | Acceptable if fits allocation |

| Bull | Margin expands, durable growth | Mid to high teens IRR | Accumulate within size limits |

Part 6: Building the Habit Loop

- Make it obvious

Put your one-page policy and rebalancing rules where you place orders. - Make it easy

Automate SIPs, rebalancing alerts, and diary prompts. Use calendar reminders. - Make it satisfying

Track “process wins”: followed policy, logged a decision memo, executed band rebalance. Celebrate consistency, not outcomes you do not control.

Part 7: When To Get Help

- Your net worth or income changed meaningfully.

- You are sitting on a large, concentrated position and taxes complicate exits.

- You repeatedly override your rules.

- You want a second set of eyes on your policy and risk guardrails.

A good advisor is a behavioral co-pilot. They do not eliminate uncertainty. They help you face it with a repeatable process.

Closing Thought

You do not need to outsmart the market every day. You need to outsmart your worst impulses often enough. Treat loss aversion, anchoring, and herding as design problems, not character flaws. Then build a system that keeps your future goals in the driver’s seat when your emotions try to grab the wheel.

Ready to turn this playbook into your personalized policy, allocation, and automation plan? We build behavior-first portfolios with clear guardrails, so your long-term goals drive every decision. If you want, I can turn the tables above into a one-page Investment Policy and a rebalancing schedule tailored to you.

Disclaimer: The information presented in this document is intended for informational and educational purposes only and does not constitute investment advice, solicitation, or recommendation to buy or sell any financial product. While every effort has been made to ensure accuracy, Wert Finserve makes no representations or warranties regarding the completeness or reliability of the data provided. Market conditions are subject to change, and past trends may not continue. Readers are advised to consult a SEBI-registered investment advisor for personalized financial guidance before making any investment decision.